How to Stop Living Paycheck to Paycheck: A Beginner’s Guide to Taking Control of Your Money

Savings & Debt Guide

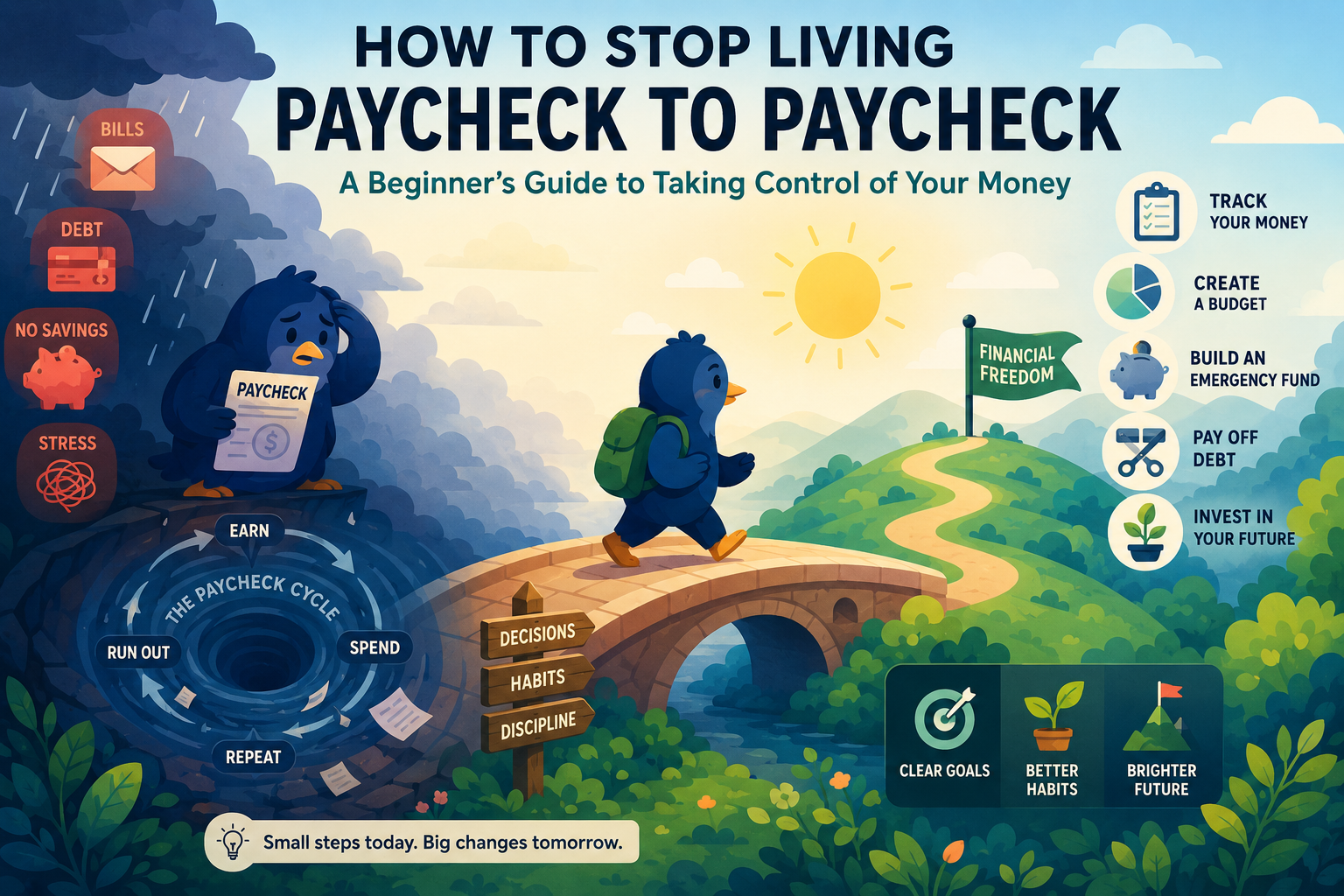

Living paycheck to paycheck means most or all of your income is gone before your next payday arrives. It can feel stressful, but it is possible to break the cycle by tracking your money, building a small buffer, reducing debt and making your income work before it disappears.

Many people live paycheck to paycheck even when they earn a normal income. The problem is not always laziness or bad habits. It can come from high bills, debt payments, rising prices, low income, irregular work, poor budgeting or simply not knowing where the money is going.

The goal is not to become rich overnight. The goal is to create breathing room. Even a small gap between your income and expenses can make life feel less stressful and give you more control over your money.

This guide explains how to stop living paycheck to paycheck step by step, even if you feel like there is no money left at the end of the month.

What you will learn

- What living paycheck to paycheck means

- Why people get stuck in the cycle

- How to track where your money is going

- How to build a small money buffer

- How to reduce bills and spending leaks

- How to deal with debt payments

- How to avoid relying on credit cards or overdrafts

- How to create a simple 30-day plan

Important:

This article is for educational purposes only. It is not personal financial advice or debt advice. If you are missing payments, struggling with priority bills or feeling overwhelmed by debt, consider speaking to a qualified adviser or a free debt support organisation in your country.

Useful official resources

Helpful outbound links:

Consumer Financial Protection Bureau: Budgeting

MoneyHelper: Budgeting guidance

MoneyHelper: Save or pay off debt?

StepChange: Free debt help

Related guides on The Trading Journal

Helpful internal links:

How to Budget Money

How to Build an Emergency Fund While Paying Off Debt

Debt Snowball vs Debt Avalanche

How to Build Credit as a Young Adult

What Is Net Worth?

What does living paycheck to paycheck mean?

Living paycheck to paycheck means you rely on your next income payment to cover your next set of bills and expenses. There is little or no money left over after rent, food, transport, debt payments and everyday spending.

This can feel risky because one unexpected cost can cause stress. A car repair, late payment, medical cost, broken phone or higher bill can push you into overdrafts, credit cards or borrowing.

Simple meaning:

If missing one payday would cause immediate financial panic, you are probably living paycheck to paycheck.

Why people live paycheck to paycheck

There are many reasons people get stuck in this cycle. Sometimes income is too low. Sometimes bills are too high. Sometimes debt payments take up too much of the budget. Sometimes spending is not being tracked properly.

- Rent or housing costs are too high

- Debt payments take up too much income

- Food and transport costs keep rising

- Subscriptions and small expenses add up

- Income is irregular or too low

- There is no emergency fund

- Credit cards or overdrafts are used to cover gaps

- Lifestyle spending rises whenever income rises

Think about it:

The problem is not always one big expense. Sometimes it is 20 small leaks that quietly drain your money every month.

Step 1: Find out where your money is going

Before you can fix the problem, you need to see it clearly. For one month, track everything you spend. Do not guess. Use your banking app, notes app, spreadsheet or budgeting app.

Split your spending into simple categories: housing, food, transport, debt, bills, subscriptions, shopping, eating out, savings and other spending.

Spending review checklist:

Check your bank statements.

Write down every subscription.

Separate needs from wants.

Look for repeat spending.

Highlight anything you forgot about.

Find the top three categories draining your money.

Step 2: Build a tiny money buffer

When you are living paycheck to paycheck, building a full emergency fund can feel impossible. So start smaller. Your first goal is not three to six months of expenses. Your first goal is a tiny buffer.

A tiny buffer could be 50, 100, 250 or 500 depending on your income and expenses. This money is not for investing or spending. It is there to stop small problems from becoming new debt.

Example:

If you save 20 per week, you could have 260 after 13 weeks. That small buffer could cover a minor emergency without using a credit card.

Step 3: Create a simple payday plan

A payday plan tells your money where to go as soon as you get paid. This is important because money without a plan disappears quickly.

When you get paid, cover essentials first, then debt minimums, then savings buffer, then flexible spending. Do not wait until the end of the month to see what is left.

No payday plan:

Spend first, panic later, save whatever is left.

With a payday plan:

Bills first, debt minimums next, savings buffer next, spending last.

Step 4: Separate bills money from spending money

One reason people run out before payday is that all the money sits in one account. Bills, food, fuel, subscriptions and spending all mix together, making it hard to know what is safe to spend.

Try separating money into different pots, accounts or categories. One pot for bills, one for food and transport, one for savings, and one for flexible spending.

Beginner tip:

If your bills money is separate, you are less likely to accidentally spend rent, insurance, phone bill or loan payment money.

Step 5: Cut the easiest spending leaks first

Do not start by trying to remove every bit of fun from your life. Start with the easiest leaks: things you pay for but do not really use, need or value.

- Unused subscriptions

- Food delivery you regret later

- Duplicate streaming services

- Bank fees you could avoid

- Impulse purchases

- Convenience spending

- Unused memberships

- Expensive phone or insurance plans you have not compared

Example:

Cutting 30 a month from subscriptions and 20 a week from impulse spending could free up over 100 a month without changing your whole life.

Step 6: Deal with debt properly

Debt can keep you trapped paycheck to paycheck because payments take money before you can save it. Credit cards, overdrafts, payday loans and high-interest debt can be especially damaging.

Make at least the minimum payment on every debt. Then focus extra money on one debt at a time. You can use the debt avalanche method by targeting the highest interest rate first, or the debt snowball method by targeting the smallest balance first.

Debt avalanche:

Focuses on the highest interest rate first. Usually saves more money mathematically.

Debt snowball:

Focuses on the smallest balance first. Can build motivation through quick wins.

Step 7: Stop using credit to fill the gap

If you use credit cards, overdrafts or buy now pay later to survive until payday, the next paycheck is already under pressure before it arrives.

The goal is to break the pattern slowly. Start by reducing how often you use credit for everyday spending. Then use your small buffer to handle minor surprises instead of borrowing again.

Important:

If debt payments are unaffordable or you are borrowing to pay bills, get support early. Waiting can make the problem harder to fix.

Step 8: Lower fixed bills where possible

Fixed bills are powerful because reducing one bill can save money every month. Even small monthly savings can create breathing room.

- Compare insurance prices

- Review phone contracts

- Cancel unused memberships

- Check broadband or internet deals

- Reduce energy waste where possible

- Meal plan to reduce food waste

- Consider cheaper transport options

- Negotiate or switch providers if suitable

Simple rule:

One bill reduced by 20 a month gives you 240 a year back. Several small reductions can make a real difference.

Step 9: Avoid lifestyle inflation

Lifestyle inflation happens when your spending rises every time your income rises. You earn more, but you still feel broke because the extra money disappears into upgrades, subscriptions, eating out or bigger payments.

When your income increases, decide in advance where the extra money will go. Put some toward savings, debt repayment or future goals before increasing spending.

Think about it:

If your income went up by 200 a month, would your financial life improve, or would your spending quietly rise by 200 too?

Step 10: Increase income if cutting is not enough

Sometimes the problem is not spending. Sometimes income is simply too low compared with essential costs. If you have already cut obvious waste and still cannot create breathing room, increasing income may be necessary.

- Ask for more hours if available

- Apply for better-paid roles

- Build a useful skill

- Sell unused items

- Take temporary overtime

- Start a small side income carefully

- Check if you are eligible for support or benefits

- Improve your CV and job applications

Be careful:

Do not start a side hustle that requires expensive upfront costs if you are already financially stretched.

A simple 30-day plan

Breaking the paycheck-to-paycheck cycle takes time, but you can make progress in the next 30 days.

- Day 1: Check your balance and list all bills

- Day 2: Write down every debt and minimum payment

- Day 3: Cancel one unused subscription

- Day 4: Set up a separate savings pot

- Day 5: Move a small amount into your buffer

- Day 6 to 10: Track every purchase

- Day 11: Identify your biggest spending leak

- Day 12 to 15: Reduce one flexible spending category

- Day 16: Compare one major bill

- Day 17 to 20: Plan meals or transport spending

- Day 21: Make a debt payoff plan

- Day 22 to 27: Avoid new credit spending

- Day 28: Review progress

- Day 29: Set next month’s savings target

- Day 30: Create your next payday plan

30-day goal:

Do not try to fix everything at once. Aim to know where your money goes, stop one leak, build a small buffer and create a better payday plan.

Common mistakes to avoid

- Trying to save whatever is left instead of saving first

- Ignoring small purchases because they seem harmless

- Using credit cards to cover normal spending

- Missing debt payments to save money

- Cutting all fun and then giving up

- Not separating bills money from spending money

- Keeping unused subscriptions

- Not building even a small emergency buffer

- Assuming a pay rise will fix everything automatically

- Waiting too long to ask for debt help

Frequently asked questions

How do I stop living paycheck to paycheck?

Start by tracking your spending, separating bills from spending money, building a small buffer, reducing waste, paying debt strategically and planning your money on payday.

What if I have no money left to save?

Start tiny. Even saving 5 or 10 builds the habit. Then look for spending leaks, bill reductions or ways to increase income.

Should I save or pay off debt first?

Many people benefit from a small starter emergency fund first, then focusing extra money on high-interest debt. But always make minimum payments on debts.

Is living paycheck to paycheck always caused by bad spending?

No. It can be caused by low income, high rent, debt, inflation, family costs, irregular work or unexpected bills. Spending habits matter, but they are not always the only reason.

How much money should I keep as a buffer?

Start with a small target such as 100, 250 or 500 depending on your situation. Later, you can build toward a larger emergency fund.

Can budgeting really help?

Yes, but only if it is realistic. A good budget shows what your money needs to do before payday arrives.

Quick recap

- Living paycheck to paycheck means your money runs out before the next payday

- The first step is tracking where your money actually goes

- A tiny emergency buffer can stop small problems becoming debt

- A payday plan gives every part of your income a job

- Separating bills from spending money can prevent mistakes

- Debt payments should be managed strategically

- Reducing bills and spending leaks creates breathing room

- Increasing income may be necessary if essentials are too high

Final thoughts

Stopping the paycheck-to-paycheck cycle is not about becoming perfect with money. It is about creating a little more control each month.

Start small. Track your spending. Build a tiny buffer. Reduce one bill. Pay one debt down. Create one better payday plan. These small steps can slowly turn financial stress into financial breathing room.

The goal is simple: stop letting payday rescue you every month. Build enough space between your income and expenses so your money starts working for you instead of constantly disappearing.